For the millions of business owners that offer a workplace retirement plan, the COVID-19 pandemic created many financial difficulties.

However, as the economic climate improves, there is an opportunity for employers to refresh their company’s retirement plan. With an important plan document restatement deadline happening in 2022, there’s never been a better time for employers to reevaluate their current plan design and, if necessary, add or update features that align with their business objectives and retirement plan goals.

Cycle 3 Deadline is Next Year

Vanguard. “Revisiting the CARES Act and its impact on retirement savings.” January 2021.Every six years, the IRS requires business owners to restate their pre-approved qualified retirement plan documents to ensure they are up-to-date and compliant with current regulatory and/or legislative changes. A restatement means the plan document must be completely rewritten to reflect mandatory regulatory changes, as well as any voluntary changes made to the plan since the last update. But don’t worry, this is very normal and nothing to fear.

The latest restatement cycle for these plans began on August 1, 2020 and will close on July 31, 2022. It’s known as “Cycle 3,” since it’s the third restatement period required under the pre-approved retirement plan program.

Since the last restatement period that ended in April 2016, there have been several legislative and regulatory changes that impact retirement plans. However, this restatement period doesn’t include regulations introduced in the Setting Every Community Up for Retirement Enhancement (SECURE) Act and the Coronavirus Aid, Relief, and Economic Security (CARES) Act. They must be addressed in separate, good faith amendments.

Restatement is mandatory. Plans that haven’t complied by the deadline could face penalties from the IRS. Even newly established or terminating plans need to restate their plan documents.

The restatement period provides employers with an opportunity to enhance their existing retirement plans — especially in light of the pandemic. Updating the plan’s design now could better position business owners, employees and companies for the future.

Plan Design Updates to Consider

Like many employers, you may be looking for ways to prepare your employees more effectively for retirement by increasing focus on plan design, investment performance and financial wellness. With these motivations top of mind, here are some plan design features worthy of consideration:

Automatic savings features: Adding auto-features like auto-enrollment and auto- escalation may improve plan participation and increase savings rates.

Auto-enrollment enables employers to automatically enroll new hires into the retirement plan. To help maximize savings and improve outcomes, employers may want to consider enrolling new employees at a higher deferral rate, such as 6%, rather than the standard 3%. Under the SECURE Act, employers that implement auto- enrollment can also receive a tax credit. Additionally, employees can always opt out if they don’t want to participate.

With auto-escalation, employees’ contributions are automatically increased every year. For example, employers can increase deferral rates by 1% each year up to a maximum of 15% of pay.

2. Matching contributions: Employers experiencing budgetary constraints may consider altering the match rather than terminating it. Instead of matching 100% of a 3% employee contribution, the employer could stretch the match, such as 25% match on a 12% contribution. It costs the same but may encourage higher savings rates since employees must increase deferrals to get the full match.

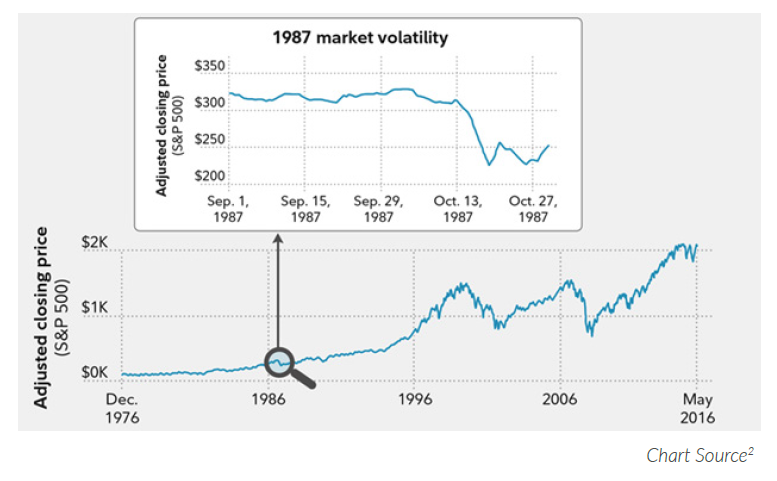

3. The investment menu: After the market volatility that dominated 2020, employers might consider reassessing the plan’s fund lineup. Reviewing the investment menu and streamlining options may help to improve diversification and returns.

4. Personalized solutions: Workers value personalized, professional retirement planning education. With personalized income solutions and investment advice more widely available, these options may be worth a conversation.

5. Financial wellness and emergency savings programs: The pandemic was a harsh reminder that many Americans are unprepared for a financial emergency. Financial wellness and emergency savings account (ESA) benefits can support employees as they get their finances back on track and may encourage them to save so they can better weather the next inevitable storm.

The pandemic presented unprecedented challenges for employers that offer retirement plan benefits. With the future looking brighter and the Cycle 3 restatement deadline around the corner, now is the optimal time for business owners to review, and if necessary, update their plan design to confirm it aligns with your company’s goals and cash flow obligations.

Contact Information:

CURTIS S. FARRELL, CFP®, AIF®

949.455.0300 x222

cfarrell@fmncc.com

ARAN SAHAGUN, CRPS®

949.455.0300 x210

asahagun@fmncc.com

Disclosures:

Investment advisory services are offered by Financial Management Network, Inc. (“FMN”) and securities offered through FMN Capital Corporation, (“FMNCC”), member FINRA & SIPC.

This information has been developed as a general guide to educate plan sponsors and is not intended as authoritative guidance or tax/legal advice. Each plan has unique requirements and you should consult your attorney or tax advisor for guidance regarding your specific situation.

© 401(k) Marketing, LLC. All rights reserved. Proprietary and confidential. Do not copy or distribute outside original intent.